At Note, we frequently encounter business owners who tell us they get approached by “wealth” managers preaching asset allocation. These managers possess little information about them, their businesses, their objectives, or the headwinds they’re facing. These managers then readily preach about the importance of diversification and the investments that owners need to make.

The thing is, most business owners aren’t thinking about asset allocation at all. Rather, they’re focused on asset concentration.

Why?

Because their life savings and sweat equity are tied up in their business. This is punctuated by the debt they’ve taken on in order to feed the engine of their business – their most concentrated investment.

While asset allocation may be wise advice from an “Investment 101” standpoint, it is not an effective conversation with most small business owners. Many I’ve spoken to over the years are quick to say, “I have nothing to invest.”

However, if I have their ear, I’m able to persuade them they have everythingto invest.

They have themselves, their tomorrows, and the investments they’ve already made. With good fortune and perseverance, those assets will give them the kind of financial capital that wealth managers very much want under their management. However, it can take a decade or two before that happens. Only then does asset allocation advice become relevant.

An effective financial advisor must be able to see you – the business owner working to build equity. They must recognize the importance of promoting asset concentration, not preaching diversification. They should fully understand your business, your objectives, and the headwinds you are facing. Only then can they be dedicated to working with you to mitigate the risks associated with business ownership. Only then can you more easily move from concentration through liquidity, and onto successful allocation.

This simple three-word phrase is one I’ve heard throughout my career, in instances that often stick in my mind. One of those relates to a couple I worked with for more than 20 years. Early on, I provided the husband with financial advice about an insurance policy, which he then purchased. Sadly, he subsequently contracted an illness that caused him to become disabled for the remainder of his life.

As I do with all clients, I attempted to get back together with the couple for an annual review of that policy, and the details of how it worked. More often than not the appointments were scheduled and cancelled as “unnecessary,” with the wife always concluding, “We’re all set.”

This year the gentleman passed away. His widow contacted me to ask if I could provide her information on his life insurance beneficiaries. When I shared the information, she was shocked. She indicated that she and her husband had modified their wills to ensure select individuals they had originally noted as beneficiaries on the policy would not receive any proceeds.

I advised her that since such a policy is a separate contract with the insurance company, changing their wills did not change the beneficiary designations. I explained that unless an insurance contract is modified, the policy is paid out according to the original terms.

At that point, the widow became upset, saying her husband would be rolling over in his grave if he knew the amount of money that would be going to certain beneficiaries. She said she understood that she and her husband had cancelled a number of appointments with me and clearly they were not as “set” as they both thought.

I advised her that I was sorry but, as difficult as it was to watch it unfold, the proceeds were being paid out exactly as they had been written. In the end, it was an expensive and painful lesson for this woman about the consequences of not being “all set.”

Medical professionals require an active relationship with their patients in order to establish and maintain a baseline of their health. Without that baseline there is no reference for how much a patient has changed, how their current health varies from “normal”, or how to ensure their ongoing wellness.

The same is true for financial professionals.

Without a baseline understanding of a client’s personal and financial situation and a game plan for the future, advising is often nothing more than business transactions that sometimes include opportunistic purposes to sell products to a client without clear objectives.

Today, professionals in every field are recognizing the risks of advising “we’re all set” clients; those who don’t proactively participate in the planning process. They are also facing increased liability costs of attempting to advise reactive individuals in today’s litigious society. Many are notifying such clients of non-compliance and pruning them from their client/patient lists. Not a great place to find yourself when you need professional help and realize you are not “all set,” not insurable, not prepared for retirement, not liquid and not protected by any kind of safety net or parachute.

The next time you’re inclined to dismiss a professional who is trying to serve you and maintain an active relationship, think twice. Agree to meet with them and keep that appointment. Maintain your baseline. Let your professional lead you through their established processes and provide you with proven solutions. Make sure that ultimately, when you say those three little words, you really are, “all set.”

In the decades I’ve spent advising individuals on their businesses and their wealth, I’ve observed that people are often concerned about having the “right answers.” It makes sense. We all want to be correct, feel affirmed, and know we’re on the path of success. However, I’ve learned that to arrive at the “right answers,” you need to ask the right questions. At Note, we believe great advisors ask great questions. The kinds of questions others might not.

Questions you never get to fully contemplate in the day-to-day demands of running your business.

Questions which, by the time you recognize they should have been asked and addressed, rob you of valued financial capital and time.

“What made you decide to start this line of work?”

“Are you still doing it for the same reasons?”

“What has to happen over the next three years for you to feel professionally fulfilled and successful?”

“When was the last time you took off a couple of weeks, or even a month, from your work?”

“If you don’t have the support in place to take a month off or more, what do you think would happen to your business if you become unable to work for an extended period of time due to illness, injury, or premature death?”

These kinds of essential business questions don’t stop there. For many business owners, there are succession concerns that can implicate partners, family, and employees.

“How do you plan on getting out of this business alive?”

“Are your children working for you? If so, do they expect to own the business someday?”

“Can you identify key employees in your company?”

“Do they know they are your key employees?”

Some business owners have shareholder involvements.

“Have you reviewed your shareholder agreement to make sure those integral to your business aren’t robbed of ownership positions, like your children?”

“How might this impact partners and co-shareholders you might have?”

“Does your shareholders agreement address liquidity needs that may occur during their lives—college education funding, unanticipated expensive medical care, helping a child with a home down payment or a grandchild with their education?”

“Can these needs create the unintended consequences of diminished business focus, or loss of a key shareholder?”

There’s also the challenge of managing relationships with varied business advisors.

“Do you have a collaborative team of advisors—an accountant, a tax expert, a lawyer, an operations pro? “How do you coordinate communication among them all?

“Do you have one core advisor facilitating such communication? Or do you find yourself spending your business time interpreting the work of each one of your advisors for everyone else?”

“How’s that working for you?”

If any of these questions hit a nerve, I want you to know that I see you and the challenges you’re facing. That’s why I’m passionate about asking great questions that grab your attention and give you pause. Questions that inspire the right answers for your family, your business, your wealth, and your legacy.

According to a recent survey, 80% of Americans say that saving for retirement is critically important. However, only 56% are actually putting money away for their golden years.

In 2006 U.S. Senators Gordon Smith and Kent Conrad introduced a resolution that was passed by Congress, creating National Retirement Security Week in the third week of October (this year October 18-24.) On September 2, 2020, the National Association of Government Defined Contribution Administrators (NAGDCA) updated its legislative priority to advocate for October to become National Retirement Security Month.

The purpose of observing National Retirement Security Week/Month is to raise awareness and help individuals take concrete steps towards a secure retirement. Over and above elevating public knowledge on the subject, there is also an effort to encourage employees to speak to a retirement plan consultant or expert and participate in an employer-sponsored retirement plan if available.

At Note Advisors, we are here to help you build and increase your retirement funds. While it can seem like an overwhelming process, here are some basic ways that you can start to secure your retirement future.

Start saving money

Statistics show that 32% of Americans did not start saving for their retirement until they were in their 30s. Another 13% waited until their 40s. The longer you wait, the greater the amount you will need to save each month, but it’s never too late. Start saving now.

Automate Your Savings

Have your contributions automatically deducted from your paycheck to guarantee that you are saving.

Boost Contributions as You Age

If you are over 50 years old, you can save an extra $6,000 per year tax deferred.

Don’t Rely on Social Security

Social Security was never meant to serve as a total retirement income replacement source It was meant to supplement pension income. Further, nearly a quarter of public sector employees are ineligible. Social Security benefits replace roughly 40% of pre-retirement income among average earners. While this is a meaningful supplement to other income sources, it’s hardly enough to maintain a comfortable lifestyle on its own.”

If You’re Young, Invest More Aggressively

Choosing a more aggressive investment strategy early will quickly grow your nest egg and also give you time to recoup if the market takes a dip.

Meet Your Company Match

If your company offers to match your contribution up to a certain percentage do it. It’s free money and that match can be tax-deductible for your employer as well. Diversify Add a tax-advantaged retirement account like a Roth IRA to your retirement portfolio, so that some of your saving grows tax free.

No Company Retirement Plan?

While 28% of Americans take full advantage of their company’s retirement saving options, 20% aren’t offered a plan by their employer, or are independent contractors. If you fall into that category, consider alternative solutions, like an Individual Retirement Account (IRA).

Speak with a retirement plan consultant or expert

Nearly 60% of Americans say they have a workable knowledge of how retirement plans operate, but 30% say they don’t have a clear vision of their own plan. If you are unsure about planning your retirement, we at GCW Capital are here to help. Contact us today and let’s work together to develop a retirement strategy that meets your needs and will fund your future.

If you are self-employed, you shouldn’t count on the payroll tax break the president has issued via executive order — at least not yet.

Payroll taxes are normally shared by employers and employees. Each covers a 6.2% tax to fund Social Security, as well as a 1.45% tax to fund Medicare.Self-employed people foot the entire bill for these levies themselves, at a cost of 15.3%, and pay for them as part of their quarterly estimated taxes

The president’s executive order would suspend the employee’s share of payroll taxes from September 1st through the end of the year. It would cover workers who make no more than $4,000 per biweekly pay period or $104,000 annually.

It is currently unclear whether this relief would apply to the self-employed, which is raising a number of tax concerns including whether employers or employees could face surprise tax consequences and compliance issues related to the executive order.

Separately, business owners, including independent contractors and freelancers, are already eligible to defer the employer’s side of the Social Security tax via the CARES Act. Under this provision, employers may choose to defer the share of tax that would have been paid from March 27 through Dec. 31. They would then pay 50% of the amount owed next year and the remainder in 2022.

With so many unanswered questions, the best course of action if you are self-employed is to continue to set aside your self-employment taxes and pay them as usual. At the very least, you should wait until further guidance is issued by the Treasury Department to decern on whether you qualify to defer this slice of the tax.

If you have questions, or need to talk about this or any other financial issues, give us a call. We’re to help

The pandemic has had a major economic impact on employers as well as individuals. According to a national survey by the Plan Sponsor Council of America, as of April more than 20 percent of large organizations had already suspended matching 401(k) contributions.

The beauty of a 401(k) is that it offers tax advantages and makes regular contributions seamless. Having a match on top of that is icing on the cake—but not having it doesn’t negate the other benefits.

When money is tight, you may have to rethink and reprioritize. You don’t want to jeopardize your future, but you also don’t want to make imprudent decisions like racking up a huge credit card bill or defaulting on other commitments in order to continue contributing.

On the other hand, if your budget still allows you to make regular contributions, you definitely should. In fact, as counter-intuitive as it may seem, now could be the time to increase your contribution to make up for the lost match.

It’s a balancing act. So, before you decide what to do, ask yourself these questions.

How Stable is Your Job?

When the company you work for, whether large or small, is looking at its balance sheet to find ways to economize, you want to be realistic about the future of that company. Are there layoffs ahead? Cutback in hours? If you think your position could be impacted, now is the time to make sure you have enough cash on hand to be able to make it financially.

Do You Have an Adequate Emergency Fund?

Today’s uncertainties have brought the importance of emergency funds front and center. The standard recommendation to have enough cash easily accessible to cover three-to-six months essential expenses may even be an understatement. If your emergency fund is less than adequate, building it up should be a primary focus.

Look at your budget. Can you redirect some dollars to this important fund? If there’s no other way to do it, you could reassess how much you’re currently contributing to your 401(k) in order to balance present financial stability with future security.

Have Your savings to Date Been Adequate?

A common employer match is 50 cents on the dollar for the first six percent of your salary. This means that if you have only been contributing up to the match, you’ve been contributing nine percent between you and your employer. That’s good, but below the 10-15 percent recommended for someone in their 20’s (an older person just beginning to save may need to contribute even more). If you’re behind in your savings already, you’ll likely have to work harder in the future to catch up.

How Close Are You to Retirement?

This is a crucial question. If you’re far from retirement, you may feel like you have plenty of time ahead to save. However, the reality is that the earlier you start saving—and the more aggressively you save—the more time you have to benefit from potential market appreciation and compound growth. Stop saving now and you will have lost the power of time. Conversely, if you’re close to retirement and still have a way to go to meet your savings goal, every dollar you save now is essential.

There’s More to Your 401k Than the Match

While getting an employer match is a definite plus—and an opportunity you never want to pass up—there’s more to it than that. Obviously stopping contributions, or temporarily reducing your percentage, would put more dollars in your pocket and potentially help ease your cash crunch. On the other hand, it’s a trade-off, not only in terms of your future security, but also your current tax situation.

If you have a traditional 401(k), your contributions are tax-deductible, which lowers your taxable income. Decrease or completely stop those contributions and you potentially increase your tax liability. You also decrease your long-term, tax-deferred earnings potential. If you have a Roth 401(k), you don’t get an immediate tax benefit, but the ability to take tax-free withdrawals in the future is huge.

It Doesn’t Have to be All or Nothing

If you need some extra money now for essential expenses or to boost your emergency fund, reducing your contribution (rather than stopping it completely) could make sense in the short term. Still it’s important to promise yourself that you will recommit to saving more as soon as things turn around.

Match or no match, when it comes to long-term retirement saving, contributing as much as you can to a 401(k) is one of the best things you can do.

This blog was excerpted from an online article by Carrie Schwab-Pomerantz, CFP®, Board Chair and President, Charles Schwab Foundation; Senior Vice President, Schwab Community Services, Charles Schwab & Co., Inc.; Board Chair, Schwab Charitable

There are many statistics about the gender pay gap worldwide. For example, in the United States, women still only earn 82 cents to a man’s dollar. It is also well acknowledged that women, on average, outlive men. So, the importance of women saving and investing to help make up for this deficit is obvious.

The thing is, according to a study conducted in the late 90s by Brad M. Barber and Terrance Odean, while women have many traits that would make them good investors, they are far less confident than men in their investing ability. In fact, data from several studies over the years show that even when women have investment accounts, they hold the majority of their money in more conservative holdings like bonds and cash.

The question becomes, how to get women not only to invest, but to invest more aggressively when appropriate. The following five tips can help.

1. Begin With an Emergency Fund

The first step to financial security is having enough cash in a savings account to cover at least three-to-six months’ worth of unexpected expenses. This fund will not only help you in case of an emergency, but can also give you the confidence to start investing and help weather a market downturn.

2. Look to retirement

Whether you’re in your 20s or your 40s, you can’t afford to wait to start saving for retirement. And even though women are known to put others’ needs first, when it comes to retirement, you have to think of yourself. Take full advantage of a company retirement plan like a 401(k). In fact, this is a great way to begin investing. Contribute at least up to the company match, more if possible. Don’t have a company plan? Consider an IRA. The point is to save as much as you can as soon as you can. Living to 90-plus is becoming more common. You need to be prepared.

3. Invest in stocks

Your first thought may be that you don’t want to take the risk. Market downturns definitely happen as we’ve recently seen, but being too cautious can also put you at a disadvantage. Stocks are an important part of any portfolio because of their long term potential for growth and higher potential returns versus other investments like cash or bonds.

As evidence, consider this statistic: a dollar kept in cash investments from from 1926 to 2019, would only be worth $22 today. That same dollar invested in small-cap stocks over those 93 year would be worth $25,688 today.1

So where to begin? Many broad-based mutual funds and exchange-traded funds make it easy to invest in a cross-section of stocks. An index fund or target-date fund can make it even easier. Using a robo advisor can also be a good way to begin. You don’t have to know a lot to start; you just need to know where to start.

4. Plan for Other Financial Goals

What are your other goals—a down payment on a home, a child’s education or a vacation? Investing a portion of your savings in stocks may help you reach those goals faster, with the caveat that money you think you’ll need in three to five years should be in less risky investments. Stock investing should ideally be long-term, understanding how much risk you can stomach, and how much risk you can afford to take.

5. Ask for Help and Advice

When you have questions, ask your benefits administrator, your broker, even a knowledgeable friend or family member—but ask. There are also lots of online investing resources to explore. Need more? Consider working with a financial advisor.

A financial advisor is sort of like a personal trainer, someone to guide you and keep you going when you might otherwise be tempted to call it quits. He or she should understand your feelings, situation, and goals. Never hesitate to ask questions, including how your advisor is paid.

No time like the present

Time is a crucial factor in investing. If you have many years ahead of you to invest—and you commit to keeping your money invested—time will likely help you weather the inevitable market ups and downs. That’s not to say you can’t start investing later in life, but keep in mind that money you’ll need in the short-term should not be in the stock market.

That said, women need to develop the knowledge base and confidence to make the most of their hard-earned savings and build financial independence through investing. It doesn’t take a lot of money; it just takes getting started. Contact Angela Hall, CFP, if you’re ready!

[1] Source: Schwab Center for Financial Research. The data points above illustrate the growth in value of $1.00 invested in various financial instruments on 12/31/1925 through 12/31/2019. Results assume reinvestment of dividends and capital gains; and no taxes or transaction costs. Source for return information: Morningstar, Inc. Based on the copyrighted works of Ibbotson and Sinquefield. All rights reserved. Used with permission. The indices representing each asset class are CRSP 6-8 Index (small-cap stocks) through 1978, Russell 2000 thereafter; and Ibbotson U.S. 30-day Treasury bills (cash investments). Past performance is no guarantee of future results.

Parts of this blog were excerpted from an online article by Carrie Schwab-Pomerantz,CFP®, Board Chair and President, Charles Schwab Foundation; Senior Vice President, Schwab Community Services, Charles Schwab & Co., Inc.; Board Chair, Schwab Charitable

Retirement. A time in life to which we all look forward. However, According to the Bureau of Labor Statistics, in 2016, 26.8% of those between the ages of 65-75 continued to work—a number that is expected to rise to 30.6% by 2026.

There are varying reasons Americans are postponing retirement, from economic stability to personal fulfillment. Whatever the reason, and however long you might plan to remain working, there are retirement-related financial concerns that should be addressed in your sixties to ease your eventual retirement transition and avoid potential snags down the road.

Wait to File for Social Security

Just because you reach “full retirement age”(FRA)doesn’t mean you have to collect Social Security benefits, especially if you’re still working. The longer you wait, the more your benefits will increase—up to age 70.

Monthly benefits increase between six and seven percent for every year you delay from age 62 to your FRA, and then grow eight percent a year between your FRA and age 70. If you are healthy and longevity runs in your family, you stand a good chance of increasing your lifetime benefit by postponing your start date.

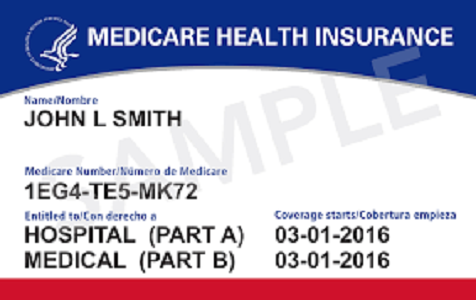

Enroll in Medicare Part A

If you’ve already filed for Social Security, you’ll be automatically enrolled in Medicare Part A and Part B at age 65. But if you haven’t, you have a choice to make.

Most people will benefit by enrolling in Medicare Part A at age 65 whether or not they continue to work. There are no premiums, and enrolling now will help you avoid potential penalties or delays down the road.

If you’re covered by your employer’s plan and your company has 20 or more employees, that plan will remain your primary coverage. If you work for a company with fewer than 20 employees, Medicare will be your primary insurer.

*Another caveat: Once you enroll in any portion of Medicare, you can no longer c*ontribute to a Health Savings Account. So if you’re relying on your HSA to boost your savings, you’ll need to postpone Medicare.

Consider Postponing Medicare Parts B and D

If you work for a company with fewer than 20 employees, you’re probably best off enrolling in Medicare Part B and Part D when you turn 65. But if you work for a larger company, you may well be better off sticking with your employer plan and enrolling in Medicare once you retire. This link to a Medicare.gov website provides information on costs and coverage that may help you make a decision.

Once you leave your job, you will generally have eight months to enroll in Part B or face a penalty. Part D also has a late enrollment penalty if you go more than 63 days without “creditable” prescription drug coverage. Creditable means that your existing insurance is expected to pay as much as the standard Medicare prescription drug coverage.

Continue to Save for Retirement

No one should ever walk away from an employer’s 401(k) match, but it makes sense to try and save more. The good news is that as long as you are working, you can continue to contribute the legal maximum ($26,000 in 2020) to your 401(k) regardless of age. If you anticipate being in a high tax bracket come retirement, you might want to consider a Roth 401(k), if available.

You can also contribute up to $7,000 to either a traditional or Roth IRA as long as you have earned income, although in 2020 Roth IRAs are restricted to those who earn less than $206,000 (combined income for a married couple filing a joint return) or $139,000 (single).

Note that the 2019 SECURE Act extended the age limit for contributing to a traditional IRA from age 70½ to 72.

Don’t Forget About Required Minimum Distributions

The CARES Act passed in March of 2020 has temporarily suspended all required minimum distributions (RMDs) for 2020, regardless of age. This includes 401(k)s and traditional IRAs.

Starting in 2021 when the CARES Act expires, we will revert back to the RMD rules established by the 2019 SECURE Act. If you did not turn 70 ½ by 2020, you can wait until the year in which you turn 72 to start taking your required distributions.

Also note that earning a paycheck means you can delay taking a required minimum distribution (RMD) from your 401(k). As long as you are working (and you don’t own more than 5% of the company), that requirement is waived until April 1 of the year you retire. There are also no RMDs for Roth IRAs at any age.

Think About Your Mortgage

Conventional wisdom says we should pay off our mortgages before we retire, but it’s important to look at your mortgage in the context of your complete financial profile. Before you rush to pay off your mortgage, especially if that involves selling securities or will reduce your liquidity, you should consult with your financial advisor.

Plan How to Turn Your Portfolio into Your Paycheck

Switching from saving to spending and depleting what you’ve worked so hard to build can be a difficult transition. Before you stop working:

Review your net worth statement to understand exactly where your stand.

Make a retirement budget and stash away a minimum of a year’s worth of cash.

Review your portfolio to make sure you have the appropriate balance of risk and safety.

Consult with your financial advisor to create a tax-efficient drawdown strategy.

It’s great to choose to work for as long as it’s financially and personally rewarding, but planning carefully for the eventual transition to retirement can make the next phase of life even more fulfilling.

This blog was excerpted from an online article by Carrie Schwab-Pomerantz, CFP®, Board Chair and President, Charles Schwab Foundation; Senior Vice President, Schwab Community Services, Charles Schwab & Co., Inc.; Board Chair, Schwab Charitable

If you are fortunate enough to have a 401(k) or other employer-sponsored retirement plan, it can be the backbone of your retirement savings. Yet there is a good case for adding an IRA to your retirement funds as it not only provides the chance to save more, it can also offer more investment choices than in an employer-sponsored plan.

The question is, which IRA is right for you?

There are two types of IRAs: a traditional tax-deductible IRA and a Roth IRA. For 2020, the annual contribution limit for both is $6,000 with a $1,000 catch-up if you’re age 50-plus. However each IRA does have an income ceiling that will determine whether one or the other is right for you.

Traditional tax-deductible IRA—–This is a good option for someone who does not have a 401(k) or similar plan, a traditional IRA is fully tax-deductible. Upfront tax deductibility plus tax-deferred growth of earnings are two of the pluses of this type of IRA. However, if you participate in an employer sponsored retirement plan such as a 401(k), tax deductibility is phased out at certain income levels based on your Modified Adjusted Gross Income (MAGI). For tax-year 2020, the levels are $65,000-$75,000 for single filers, $104,000-$124,000 for married filing jointly.

Roth IRA—With a Roth IRA, you don’t get any upfront tax deduction, but you do get tax-free growth plus tax-free withdrawals at age 59½ as long as you’ve held the account for five years. And there’s no restriction if you participate in an employer plan. However, there are income phase-out limits based on your MAGI that determine whether you’re eligible to open and how much you can contribute to a Roth. In 2020, the limits are $124,000-$139,000 for single filers, $196,000-$206,000 for married filing jointly.

There are a couple of other things to considerwhen choosing between IRAs, the main one being whether you believe you will be in a higher or lower tax bracket when you retire.

That’s because withdrawals from a traditional IRA are taxed at ordinary income tax rates at the time of withdrawal; qualified Roth withdrawals are tax-free. Also there’s no required minimum distribution (RMD) for a Roth, but with a traditional IRA, you’ll have to begin taking an RMD at age 70½, or 72 if you were born on or after July 1, 1949.

Whether or not you choose to open an IRA, if your employer offers a Roth 401(k), you might also consider adding this to your retirement savings strategy. There are no income limits to participate in a Roth 401(k), and you can have both types of 401(k) at the same time.

Having both doesn’t mean you can contributemore than the total annual 401(k) contribution limit, but you can split your contributions between the two, giving you a combination of both taxable and tax-free withdrawals come retirement time. Making your 401(k) and IRA work together.

The goal of all this is to give you the greatest opportunity to save, with the greatest flexibility. Contribute enough to your 401(k) to capture the maximum company match, then, if you’re eligible contribute to a tax-advantaged Health Savings Account (HSA). If your 401(k) has limited investment options consider opening either a traditional or a Roth IRA and contribute the annual maximum.

Next, if you can, put more money in your company plan until you max it out. And if you get to the point where you can save even more (kudos!), put that money in a taxable brokerage account. The bottom line is you can’t really save too much, only too little.

Use all the savings and investing vehicles available to you, including both an IRA and your 401(k), to save as much as you can, as early as you can—and, at the same time, get the maximum tax break. You won’t regret it.

This blog was excerpted from an online article written by Carrie Schwab-Pomerantz, CFP®, Board Chair and President, Charles Schwab Foundation; Senior Vice President, Schwab Community Services, Charles Schwab & Co., Inc.; Board Chair, Schwab Charitable.

If someone asked you to rate your financial know-how on a scale of 1-7 (with 7 being the highest) where would you place yourself?

If you are like the Americans who participated in the 2018 Financial Investor Regulatory Authority(FINRA) National Financial Capability Study (NFCS), you would probably give yourself a pretty high score.

In that study, 76% of respondents placed themselves in the 5-7 range. The reality is that only 34% of those who participated could correctly answer at least four of five basic financial literacy questions on topics such as mortgages, interest rates, inflation and risk.

Curious about your own answers? Here’s your chance.

Click on this link at the bottom of this post to take the Financial Literacy Quiz. It not only gives you an immediate score, it shows you how you compare to others in your state.

Whether the quiz confirms your knowledge or serves as a personal wake-up call, the generally low results of the NFCS definitely demonstrate the need to improve financial literacy in our country. The good news is that there’s tangible proof that financial education works.

According to the 2018 NFCS, nearly half of Americans (49%) who have received more than ten hours of financial education report spending less than they earn, compared with 36% of people who received less than ten hours of financial education.

Results from the PISA assessment show that young people and adults in both developed and emerging economies who have been exposed to high quality financial education are more likely than others to plan ahead, save and engage in other responsible financial behaviors.

The good news is that whether you are a parent, a teacher, an employer or a concerned member of your community, there are things you can do to help promote financial education for everyone in your community.

The Global Financial Literacy Center offers FastLane, with practical ideas and action plans for groups and individuals.

On CheckYourSchool.org, you can find the schools in your area that offer financial education and the ways you can start/reinforce local financial literacy programs.

DonorsChoose offers lesson plans and activities for educators that have been created by teachers in the field, for teachers. There are also opportunities to find school programs in your own community that you can support.

At the end of the day, there is a growing global awareness that financial literacy is an essential life skill that means not only greater prosperity, but better choices, increased confidence, and the ability to more successfully handle real-life financial challenges.

Financial literacy isn’t just about math. It is about attaining the knowledge and skills to confidently manage our everyday financial lives and the need for financial education, which is greater than ever locally, nationally, and globally

Parts of this blog were excerpted from an onlne post by Carrie Schwab-Pomerantz,CFP®, Board Chair and President, Charles Schwab Foundation; Senior Vice President, Schwab Community Services, Charles Schwab & Co., Inc.; Board Chair, Schwab Charitable