Over the last three months at Note, we have been engaged in virtual meetings with clients, working on ways to sustain their businesses in these trying, pandemic times.

Although a crystal ball might seem like the most needed tool in our advisor’s arsenal right now, here are some “good business” fundamentals we regularly share with clients that are important in any economy.

Hire the Best CPA, Attorney and Financial Advisor you can afford. Anything less can often become a big expense. Along the same lines, free advice often proves to be the most expensive.

Accumulate cash for opportunities and challenges. Keep in mind that other’s challenges may become your business opportunity.

Define the Core Values of your business and communicate them to all involved. Make sure to deliver customer service that clearly supports those values

Examine how to WOW your customer in a way that Amazon-at-your-door cannot.

Invest in the best employees you can attract.

Empower your employees to make decisions. Give them a budget for fixing mistakes and providing the highest level of service in their customer interactions.

Ask someone brutally honest and unfamiliar with your business or services to act as a customer and then grade their experience.

If you have questions or concerns about your business or need to discuss COVID-19 financial issues, we are here to help. Please contact Sarah Neuner at sarah@noteadvisor.com or (716) 256-1682 to make an appointment to meet in our office, via phone or virtually, online.

Have you ever noticed an unauthorized withdrawal from your bank, brokerage, or credit card account? Such suspicious activity can mean only one thing: Your finances have been invaded.

If this has happened to you, know you are not alone. According to a November, 2019 Nilson Report, “Credit card fraud losses in 2018 reached $27.85 billion.

The good news is that if you find yourself the target of financial fraud, there are steps you can take to limit losses and help prevent unauthorized activity from happening again.

1. Act fast

It’s in everyone’s interest to identify suspicious activity as soon as it surfaces. Your financial institution can freeze the compromised account, issue a new card, reset a password, and perhaps even help track down those responsible. Be sure to initiate contact through a known number or website; never respond to an unsolicited email, phone call, or text—no matter how legitimate it may seem.

Financial institutions generally have security policies that outline how they handle fraud—including your liability, if any, in the event of unauthorized activity.

Viruses and malware are commonly tied to fraud schemes. Indeed, if a virus is left unchecked it can capture your new username and password, even if it was changed after the initial breach.

2. Go wide

Whenever you spot fraud in one account, change the credentials on any other accounts with the same usernames and/or passwords. Better yet, assign a unique password to each financial account, as well as every site where you store bank account or credit card information.

Of course, it can be difficult to keep all those passwords straight. Password managers, such as Dashlane and LastPass, can generate a unique password for every account, keep track of them all, and even securely auto-populate username and password fields.

3. Stay Alert

In addition to fraud alerts, many credit card issuers can notify you when they process online or over-the-phone transactions that don’t require a physical card. In 2018, such transactions accounted for 54% of all fraudulent activity worldwide involving credit, debit, and prepaid cards. Bank and brokerage accounts also offer alerts and notifications for certain types of transactions.

Regularly review your statements and credit report to ensure no fraudulent activity flies under the radar. Each of the three major credit reporting agencies (Equifax, Experian, and TransUnion) is required to provide one free credit report annually, so consider requesting a report from one of the agencies every four months.

Placing a security freeze with Experian, TransUnion, or Equifax can prevent others from opening a new credit card or loan in your name. Better yet, place a freeze with all three agencies to ensure maximum protection. If you need to apply for credit in the future, you can temporarily lift the freeze using a password or PIN.

4. Double up

Activate two-factor authentication: This safeguard, now standard among financial firms, issues a single-use code via email or text that you need to enter along with your username and password to gain access to your account.

Enable biometric recognition: Biometrics let you unlock a device or log in to an account with your face, fingerprint, or voice. Unlike passwords, biometrics can’t be written down (or lost) and are much harder for criminals to replicate.

Go the extra mile

In addition to the above four steps, consider reporting your experience to TheFederal Trade Commission. The agency’s reporting process isn’t designed to resolve individual incidents or recover funds, but your report helps them track trends in fraud and better understand the methods criminals are using, which may help financial firms improve their defenses.

It’s also a good idea to file an Identity Theft Report at identitytheft.gov. This entitles you to extra protections, such as placing an extended fraud alert on your credit report and preventing companies from collecting debts that result from identity theft.

According to the NYS Department of Labor, more than 1.6 million residents have filed for unemployment benefits since Gov Cuomo’s mid-March COVID-19 order for all non-essential retailers and businesses to close.

This reality has forced business owners to make tough decisions about a broad range of issues including employee and customer safety, changes in supply chains and remote technology capabilities—all the while working to keep their businesses operational and afloat.

For more than 30 years, CEL has provided individualized and interactive education in entrepreneurship through a variety of programs aimed at unlocking leadership potential, creating jobs and invigorating the greater Western New York economy and community.

That longterm purpose led CEL to immediately begin creating virtual programs and support for their entrepreneurs in less than 48 hours following the Governor’s business shut down order. Programming includes weekly Zoom meetings and one-on-one consulting sessions on financials and other COVID-related challenges. As well there are weekly webinars pn a variety of topics such as human resources, operations and overall business strategies.

Note Advisors Principal, Shawn Glogowski, is a graduate of the CEL Program. He notes the immediate response and support offered by the organization as crucial during this pandemic.

“It’s good to see CEL react with such immediacy in helping the Buffalo business community stay the course and meet the many challenges we are all facing. The vital information on programs and next step actions they are providing definitely help to build confidence among business owners in that the decisions they are making in these uncertain times will help them survive and eventually reopen.”

Established in 1987, the Center for Entrepreneurial Leadership in the University at Buffalo School of Management provides participants with individualized and interactive education in entrepreneurship. More than 1,400 CEL alumni employ more than 23,000 Western New Yorkers, and their businesses are worth more than $2.3 billion to the local economy.

For more information on the variety of programs offered through the CEL, how these programs are providing support for local small to medium-sized businesses and how you can apply for a specific program, visit http://mgt.buffalo.edu/cel.

Some information in this post was excerpted from an online Business First article written by Tom Ulbrich, an executive in residence for entrepreneurship at the University at Buffalo School of Management, and president/CEO of Goodwill of WNY.

The current low interest rates can make it a great time for some homeowners to refinance. What’s important to note is that changes in interest rates affect fixed and adjustable mortgages differently.

While adjustable rate mortgages may be affected by short-term rate changes, fixed mortgage rates tend to be more closely aligned with the 10-year Treasury note.

If you have an ARM, a decrease in the short-term federal funds rate may lower your rate. If you have a fixed-rate mortgage, you should instead pay attention to long-term bonds like the 10-year Treasury note.

Rates aside, deciding whether or not to refinance depends on a number of personal factors.

WHAT’S YOUR GOAL?

Do you want to lower your monthly payment? Reduce the length of your mortgage? Take out extra money for home improvements? These are important initial questions.

If decreasing your payment is a top priority and you can lower your interest rate by .5 to 1 percent, it’s probably worth the effort. For instance, lowering the interest rate on a $350,000 30-year fixed mortgage by 1 percent could lower your monthly payment by about $300 a month.

On the flip side, if your goal is to shorten the length of your mortgage and you refinance that amount for 15 years, your monthly payment would go up, but you’d save a considerable amount in interest over the life of the loan.

HOW LONG WILL YOU BE IN THE HOUSE?

Refinancing usually involves paying points and fees. Points basically represent interest you pay upfront to get a lower rate on your loan. It’s not uncommon for points and fees to add up to 3-6 percent of your loan. You can pay this out of pocket or, often times, add them to the balance of your loan.

However you pay them, it will take time to get to the breakeven point where these additional costs are offset by the lower rates, so you have to think realistically about how long you intend to be in your home. If you plan to sell in the near future, the extra cost of refinancing may outweigh the monthly short-term savings.

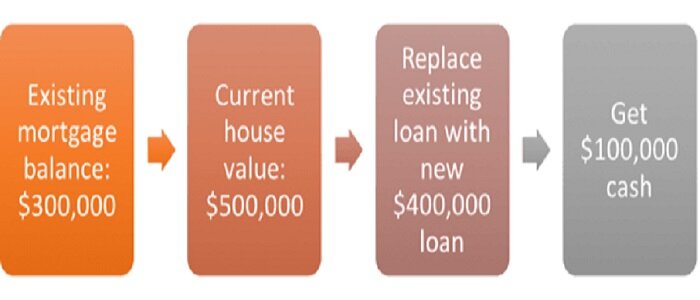

HOW MUCH HOME EQUITY DO YOU HAVE?

Do you want to lower your monthly payment? Reduce the length of your mortgage? Take out extra money for home improvements? These are important initial questions.

If decreasing your payment is a top priority and you can lower your interest rate by .5 to 1 percent, it’s probably worth the effort. For instance, lowering the interest rate on a $350,000 30-year fixed mortgage by 1 percent could lower your monthly payment by about $300 a month.

On the flip side, if your goal is to shorten the length of your mortgage and you refinance that amount for 15 years, your monthly payment would go up, but you’d save a considerable amount in interest over the life of the loan.

DO THE MATH

Refinancing usually involves paying points and fees. Points basically represent interest you pay upfront to get a lower rate on your loan. It’s not uncommon for points and fees to add up to 3-6 percent of your loan. You can pay this out of pocket or, often times, add them to the balance of your loan.

However you pay them, it will take time to get to the breakeven point where these additional costs are offset by the lower rates, so you have to think realistically about how long you intend to be in your home. If you plan to sell in the near future, the extra cost of refinancing may outweigh the monthly short-term savings.

Refinancing usually involves paying points and fees. Points basically represent interest you pay upfront to get a lower rate on your loan. It’s not uncommon for points and fees to add up to 3-6 percent of your loan. You can pay this out of pocket or, often times, add them to the balance of your loan.

However you pay them, it will take time to get to the breakeven point where these additional costs are offset by the lower rates, so you have to think realistically about how long you intend to be in your home. If you plan to sell in the near future, the extra cost of refinancing may outweigh the monthly short-term savings.

This post was excerpted from an online article by Carrie Schwab-Pomerantz, Board Chair and President, Charles Schwab Foundation, Senior Vice President, Charles Schwab & Co., Inc. and Board Chair, Schwab Charitable

In 2011, a LinkedIn Group led by a man named Joe Paris formed The Operational Excellence Society. The society’s goal is operational excellence by design over coincidence.

A significant impact of this group has been the universalization of the catchphrase “Words Matter.” It’s a simple concept that has encouraged international awareness of how the words we say and how we say them have far-reaching effects, often in ways we may never know.

Over the last three weeks, “Words Matter” has guided me through this new world order in which we are living and working. It’s been a time of stress, challenge, worry and, every once in a while, laughter. Most centrally it’s been a time of choosing words that matter as I have counseled, advised and spoken with family, friends and clients. Through each day’s experiences, this is what I have learned and relearned.

I love what I do every day, but especially when I can help clients through challenging times like the one we are now facing. I’ve been asked a lot lately how I’m dealing with the huge influx of COVID-19 calls from clients concerned about their investments and the roller coaster market. My answer is always the same. I truly enjoy engaging in conversations where I can calm people’s fears and help manage their worries.

Words matters. Clients turn to all of us at Note Advisors as confident voices in times of “noise” and turmoil. Staying positive and giving sound advice is what our clients need and deserve. It’s a purpose that we honor.

People with a financial plan in place are far less anxious than those without one. Enough said!

Retirement plans that we’ve designed for our clients are working exactly as intended. People are able to take their needed monthly income while leaving the principal of their investments in the market to recover. Planning plus thoughtful execution equals positive results.

For younger clients who think this is the time to stop investing in their 401k or IRA, it’s been rewarding to educate them on increasing their 401k deferrals and putting long term cash to work right now. It’s a huge step in positively shaping their financial outlooks and their futures.

Helping all of our clients understand the volatility of the COVID-19 stock market and encouraging them not to make reactive changes is leading to long term positive impacts on their financial futures. It is also developing stronger partnerships between us, as advisors, clients and individuals, as we face this crisis together.

The value we, as financial advisors, provide in uncertain times truly makes a difference in the lives of our clients. We are working to develop bonds of mutual respect and trust that are impacting their financial security as well as their personal well being.

As we continue to find ways to manage and move forward in this time of quarantine and social distancing, all of us at Note look forward to hearing from you—to listen to your concerns, hear your questions and partner with you in managing your human, social and financial capital.

In the meantime, because words matter: Stay safe. Stay well. Stay in touch.

To contact Shawn or any Note Advisors team member, call 716-256-1682

Shawn C. Glogowski, CFP® is a CERTIFIED FINANCIAL PLANNER™ practitioner and Principal/Chief Compliance Officer for Note Advisors, LLC. He is responsible for helping clients create, implement, and monitor their comprehensive financial plans and is truly passionate about the planning process and educating clients on investment, tax, retirement, and estate strategies to meet their needs.

Shawn holds a Chartered Financial Consultant (ChFC), Chartered Special Needs Consultant (ChSNC), and Chartered Life Underwriter (CLU) designations with The American College. He is also an Enrolled Agent with the IRS which allows him to represent taxpayers before the Internal Revenue Service.